Data Center Site Selection in Ohio: The PJM Power-Constraint Playbook

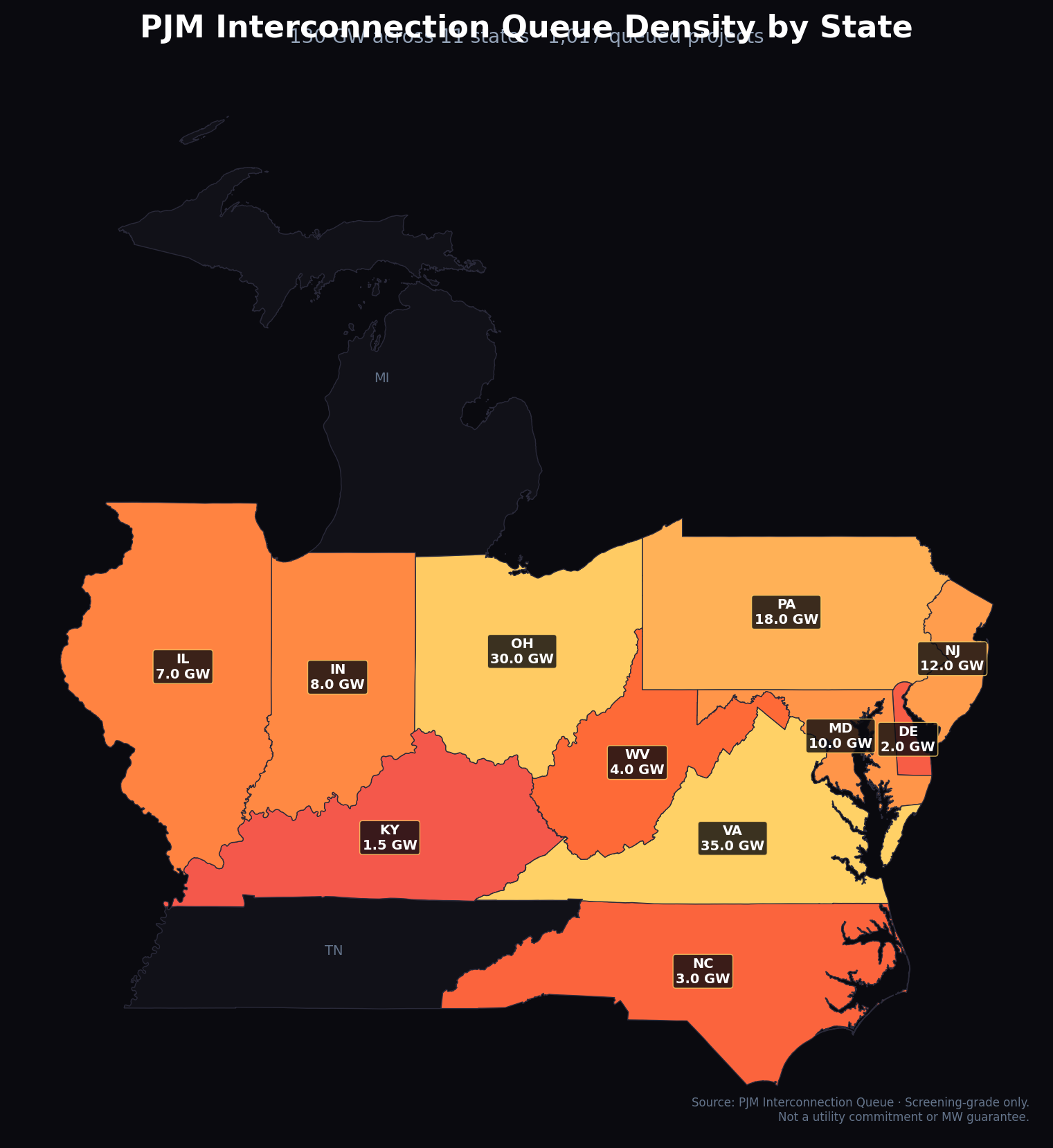

AEP Ohio has 30+ GW of service inquiries from 50+ customers. PJM's queue holds 130+ GW. The 85% minimum bill ratchet changed the economics. Columbus is the #3 US hyperscale cluster — and 18+ municipalities are pushing back.

How do you select a data center site in Ohio?

Start with AEP Ohio grid capacity and PJM queue position. Screen for 765kV transmission proximity, Data Center Tariff compliance (85% minimum bill ratchet for 12 years), water availability in Central Ohio, and local moratorium status. Columbus/New Albany is the #3 US hyperscale cluster with 200+ data centers and $40B planned investment through 2030.

Key Data Points

- PJM Queue: 130+ GW backlog, 8+ year avg interconnection timeline

- AEP Ohio: 30+ GW service inquiries, 50+ customers queued

- Data Center Tariff: 85% minimum bill ratchet for up to 12 years

- Capacity Auction: $329-333/MW-day (10x increase in 2 years)

- Investment: $40B planned through 2030 (AWS, Google, Meta, QTS)

- 18+ municipalities with active or pending DC moratoriums

Why PJM's Queue and AEP's Tariff Define Ohio Site Selection

130+ GW PJM Queue Backlog

PJM's interconnection queue holds over 130 GW of capacity-eligible projects. Average time from request to operation has grown from under 2 years (2008) to over 8 years (2025). Only 17 GW received draft interconnection agreements from the first transition cluster.

Source: PJM Interconnection Queue public export · as of 2026-04-25

30 GW AEP Service Requests

AEP Ohio has received interconnection inquiries totaling 30+ GW from 50+ customers, mostly data centers. DC load grew from 100 MW (2020) to 600 MW (2024) and is forecast to reach 5 GW by 2030. New service was paused March 2023-July 2025.

Source: AEP Ohio PUCO filings & earnings transcripts · as of 2025 Q4

85% Minimum Bill Ratchet

Ohio's Data Center Tariff (effective July 2025) requires facilities over 25 MW to pay for at least 85% of contracted capacity for up to 12 years, regardless of actual usage. This shifts infrastructure cost onto operators and fundamentally changes project economics during ramp-up.

Source: PUCO Case No. 23-0023-EL-ATA · as of 2025-07

$329/MW-day Capacity Price

PJM's 2026/27 capacity auction cleared at the FERC cap of $329/MW-day across the entire footprint — a 10x increase from $29/MW-day just two auctions prior. Total capacity bill: $16.1B. The 2027/28 auction cleared at $333/MW-day.

Source: PJM BRA auction results · as of 2025-12

The 5-Filter Site Screening Framework

Ohio's regulated tariff, PJM queue congestion, and municipal moratoriums create a three-way constraint. Screen in this order.

- 1

AEP 765kV Transmission Proximity & Headroom

Identify sites within 5 miles of AEP Ohio's 765kV backbone or 345kV substations with available withdrawal capacity. AEP's high-voltage transmission system is Ohio's key differentiator, but most substations near Columbus are nearing capacity. Sites beyond the 765kV corridor require costly transmission extensions adding 2-4 years.

- 2

PJM Queue Position & Cluster Study Status

Verify queue position within PJM's clustered study process. The first transition cluster (TC1) studied 40 GW and issued 17 GW in draft interconnection agreements. TC2 is underway. Projects entering the 2026 cycle face downstream impacts from transition upgrades. Average interconnection timeline now exceeds 8 years — queue position is a multi-billion-dollar variable.

PJM Queue Deep Dive - 3

Data Center Tariff & 85% Ratchet Compliance

Model the financial impact of AEP Ohio's Data Center Tariff requiring 85% minimum monthly billing demand for up to 12 years. Facilities over 25 MW must commit to contracted capacity regardless of utilization. Behind-the-meter generation faces additional regulatory scrutiny. This filter eliminates projects that cannot absorb the ratchet during ramp-up.

- 4

Water Availability & Municipal Moratorium Check

Central Ohio faces 56 projected instances where water demand outstrips supply by 2040. Large DCs consume up to 5M gallons/day. Columbus is building a $1.6B fourth water treatment plant (5-year timeline). Critical: 18+ municipalities have enacted or are considering data center moratoriums. Verify local zoning and water allocation before site control.

- 5

PJM Capacity Auction Cost & Incentive Stack

Layer PJM capacity costs ($329-333/MW-day) against Ohio's incentive stack: 5.75% sales tax exemption on DC equipment, 75% property tax abatements (15-30 years), JobsOhio grants, and TIF financing. Ohio DCs have claimed $2.5B in tax incentives since 2017. The sales tax exemption survived a 2025 legislative repeal attempt (governor veto) but faces ongoing political risk.

Compare PJM vs ERCOT Markets

Ohio Markets Compared: Where the Capacity Actually Is

New Albany is saturating. The question is where Central Ohio's next cluster forms — and which sites have AEP Ohio capacity and community acceptance to support it.

| Market | Capacity | Queue Depth | Time-to-Power | Notes |

|---|---|---|---|---|

| Columbus / New Albany | 600+ MW operating, 5 GW forecast by 2030 | Deep — AEP constrained, 50+ customers queued | 36-60 months | #3 US cluster. Meta 1 GW, Google 3 campuses, AWS 5 buildings. Land: $120K-$790K/acre. |

| Dublin / Hilliard (West Columbus) | 200+ MW operating | Moderate — AEP west corridor | 24-42 months | Cologix, Flexential presence. More affordable than New Albany. AEP 345kV access. |

| Licking County (Newark / Pataskala) | Under construction | Moderate — greenfield expansion zone | 24-36 months | Intel $20B fab adjacent. Land prices rising fast. Google 85-acre acquisition. |

| Cincinnati / SW Ohio | 150+ MW operating | Lower — Duke Energy Ohio territory | 18-30 months | Duke Energy (not AEP) — avoids Data Center Tariff. Iron Mountain, CyrusOne. |

| Emerging (Southern Ohio / Appalachia) | Planned only | Early stage — DOE site opportunities | 36-60 months | Portsmouth DOE site (500K sf proposed). Pike County $33B DC + power. Cheap land. |

The Numbers That Matter

Land

- New Albany premium: $120K-$790K/acre (up from $70K in 2022)

- ~3,000 acres sold to DC developers since 2021, ~$700M total

- Licking County: $40K-$80K/acre (rising fast, Intel effect)

- Southern Ohio greenfield: $5K-$15K/acre (limited infrastructure)

Power

- AEP Ohio: 765kV backbone, 600 MW DC load today, 5 GW forecast 2030

- PJM capacity price: $329-$333/MW-day (10x increase in 2 years)

- AEP service queue: 50+ customers, 30+ GW of requests

- Duke Energy Ohio (Cincinnati): separate territory, no AEP tariff

Water

- 56 projected demand-exceeds-supply instances by 2040

- Large hyperscale facility: up to 5M gallons/day cooling demand

- Columbus building $1.6B fourth water treatment plant (online ~2031)

- Air-cooled designs gaining traction in constrained areas

Incentives

- Sales tax exemption: 5.75% on DC equipment (survived 2025 veto)

- Property tax: 75% abatements for 15-30 years via PILOT/TIF

- JobsOhio: discretionary grants + job creation tax credits

- $2.5B in state/local incentives claimed by DCs since 2017

From Screening to Shortlist: The Ohio / PJM Time-to-Power Pack

This guide gives you the framework. The pack gives you the data. Move from broad Ohio/PJM screening to a curated shortlist that filters queue-heavy noise into actionable candidates.

Ohio / PJM Time-to-Power Pack

Curated Ohio / PJM shortlist built to filter queue-heavy noise into actionable siting candidates.

What you get

- Curated Ohio / PJM ranked site dataset

- Queue, curation, and readiness context fields

- Export-ready diligence package structure

Also included with your purchase

- Readiness Explorer

- Watchlists Workspace

- Standard Exports

Decision support only. Not a utility commitment, parcel-level MW guarantee, interconnection guarantee, or permitting guarantee.

One-time purchase. Self-serve checkout. No calls or demos required. Pack outputs generate immediately after unlock in GLRI.

The pack gives the current view. The Watchlist tracks what changes after.

Queue positions shift. Moratoriums expand. Capacity auctions reprice. Use the Speed-to-Power Watchlist ($99/mo) to monitor your shortlist with live readiness signals, threshold alerts, and recurring exports.

Frequently Asked Questions

How long does PJM interconnection take for data centers in Ohio?

PJM interconnection timelines have grown from under 2 years in 2008 to over 8 years in 2025. The queue holds 130+ GW of capacity-eligible projects. PJM's first transition cluster (TC1) studied 40 GW and issued 17 GW in draft interconnection agreements. Projects entering the 2026 cycle face downstream impacts from transition upgrades still being completed.

What is AEP Ohio's Data Center Tariff?

Effective July 23, 2025, AEP Ohio's Data Center Tariff requires new facilities larger than 25 MW to pay for at least 85% of their contracted electricity capacity for up to 12 years, regardless of actual usage. This "minimum bill ratchet" ensures AEP recovers infrastructure investment costs. The tariff was approved by PUCO after contested proceedings involving Google, Amazon, Microsoft, and Meta.

What tax incentives does Ohio offer for data centers?

Ohio provides three primary incentive layers: (1) a 5.75% state sales tax exemption on eligible data center equipment, approved by the Ohio Tax Credit Authority; (2) local property tax abatements of up to 75% for 15-30 years via PILOT agreements and TIF financing; and (3) JobsOhio discretionary grants and job creation tax credits. Data centers have claimed $2.5B in combined incentives since 2017. The sales tax exemption survived a 2025 legislative repeal attempt after a gubernatorial veto.

How much land do you need for a data center in Ohio?

Single-building facilities require 20-40 acres minimum. Hyperscale campuses in New Albany span 70-200+ acres (Vantage: 70 acres, Microsoft: 200 acres). Land prices in New Albany range from $120K to $790K per acre, up from $70K in 2022. Approximately 3,000 acres have been sold to data center developers in Columbus since 2021, totaling nearly $700M. Licking County offers $40K-$80K/acre but prices are rising due to the Intel effect.

Is water availability a risk for Ohio data centers?

Yes, and growing. Central Ohio faces 56 projected instances where water demand outstrips supply by 2040 according to the Ohio Chamber of Commerce. Large data centers can consume up to 5 million gallons of water per day for cooling. Columbus is investing $1.6 billion in a fourth water treatment plant in Delaware County, expected online around 2031. Air-cooled and hybrid cooling designs are increasingly favored.

Are Ohio municipalities blocking data center development?

Approximately 18 municipalities across Ohio have enacted or are considering moratoriums on data center construction as of early 2026. Concerns center on water consumption, electricity rate impacts (10-35% supply price increases reported), limited permanent job creation (as few as 10-50 per facility), and agricultural land conversion. Developers should verify local zoning, moratorium status, and community sentiment before committing to site control.

How does Ohio compare to Virginia for data center development?

Northern Virginia (Loudoun County) remains the world's largest data center market but faces severe power constraints from Dominion Energy. Ohio/Columbus offers cheaper land (outside New Albany), available AEP 765kV transmission backbone, and $2.5B in proven incentive programs. Both operate in PJM territory. Ohio's challenge is the 85% tariff ratchet and growing municipal opposition. Cincinnati (Duke Energy territory) avoids the AEP tariff entirely.

Known limitations

- —PJM queue (130+ GW) includes generation, storage, and hybrid — not all is load-side capacity.

- —AEP service inquiry volume (30 GW) is self-reported; actual committed load is a fraction.

- —85% ratchet tariff applies to AEP Ohio territory only — Duke Energy Ohio (Cincinnati) has separate terms.

- —Capacity auction prices are backward-looking; future auctions may clear differently.

- —This page is decision-support research. It is not a utility commitment, engineering study, or legal opinion.

Related Guides

PJM vs ERCOT for Datacenters

Compare queue timelines, capacity costs, and grid reliability.

PJM Queue Deep Dive

Full analysis of PJM interconnection backlog and reform timeline.

Texas Site Selection Playbook

ERCOT queue analysis and power-first framework for Texas.

Georgia Site Selection Guide

Southern Company grid access and Atlanta corridor analysis.